By Mark Sprague, Independence Title’s Director of Information Capital

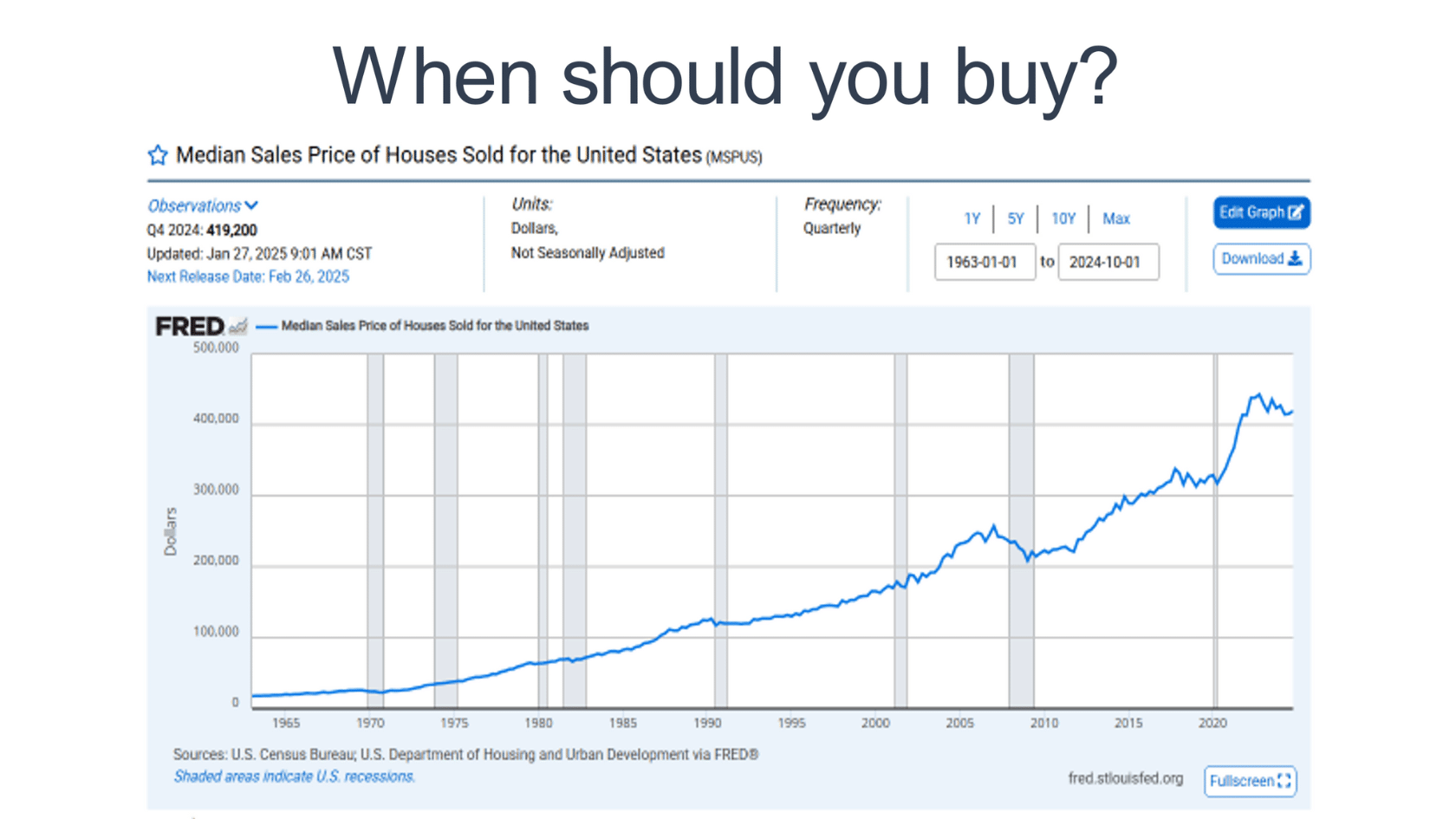

When should I buy? You should have bought 5 years ago! Five years from now, you should have bought 10 years ago. What about rates? If rates drop by .5 to .75 points, you can benefit from a refinance.

No one can time the market perfectly. As they say, “The market dictates to you.”

If you’re serious about investing in real estate, you already know that home values and interest rates have slowed after strong appreciation over the last 5+ years. And for those hoping for a reversal, both have slowed in the current economy. Values won’t drop dramatically in the Texas markets unless we get a surge in inventory. Consider the annual appreciation, which has been steadily increasing over the past decade. Appreciation is slowing, but that is not creating the significant discounts/price drops you were hoping for. A heavily discounted market is not in the cards for Texas, given the job/population growth over the last five years.

I’ve tracked and studied real estate for 50+ years, and I’ve seen how shifts in the market can either create opportunities or wipe out unprepared investors/buyers. The 2025-2026 real estate market outlook is no different.

Some buyers are panicking, pulling out of the market, and sitting on the sidelines waiting for rates or values to drop. But here’s the truth: savvy investors adjust their strategies and find ways to profit no matter what the market throws at them.

Let’s start with rates:

In late September 2025, mortgage rates were slightly higher, breaking a recent downward trend after the Federal Reserve’s recent rate cut. While rates briefly dipped after the Fed’s policy change, they are now climbing again, with 30-year fixed rates around 6.7% and 15-year fixed rates near 6.09%. This trend is influenced by factors such as the 10-year Treasury yield and bond market conditions, not just the Federal Reserve’s short-term interest rates. Key details:

- Trend Reversal: Following a brief period of declining rates, the average 30-year fixed mortgage rate has risen.

- Federal Reserve: Although the Federal Reserve cut its benchmark rate, this action has a less direct impact on fixed mortgage rates, which are more closely tied to the 10-year Treasury yield. (And multiple reasons fed funds rate should rise.)

- Economic Factors: Bond market investors’ expectations for the economy and inflation continue to influence mortgage rates.

- What about Freddie Mac/Fannie Mae going private?: Experts predict that the privatization of Fannie Mae and Freddie Mac could initially lead to an increase in mortgage interest rates. Some analysts estimate rates could rise by 0.5 to 1 percentage point immediately following privatization. Others suggest a smaller increase of 0.25 to 0.5 percentage points in the first six to twelve months as the market adjusts. This potential increase is largely attributed to the removal of the government’s implicit guarantee, which could cause investors to demand a higher return on mortgage-backed securities to compensate for the increased risk. Without this guarantee, the goal of privatized entities might shift towards shareholder profit, potentially resulting in stricter lending standards, higher fees, and higher interest rates for borrowers.

- Why conflicting indicators: The Federal Reserve’s actions affect short-term rates and variable-rate loans, but fixed mortgage rates are influenced by the market for mortgage-backed bonds, which react differently.

- Where have rates been, where are they headed: The Federal Funds Rate, a key benchmark, began rising in early 2022 from a low point of 0.05 percent in April 2020 (following pandemic-related cuts) and reached 5.33 percent by August 2023. This was a series of rate hikes aimed at cooling inflation.

- The Federal Reserve held rates steady for over a year before initiating rate cuts in the latter half of 2024. The first rate cut since December 2024 occurred on September 17, 2025, lowering the Federal Funds Rate by a quarter percentage point to a range of 4.00% to 4.25%. Mortgage rates followed.

- 30-year fixed mortgage rates surged from a low of 2.65% in January 2021 to a high of 7.79% in October 2023. As of September 17, 2025, the 30-year mortgage rate averages 6.30%. These rates have experienced fluctuations, including a dip in September 2024 and September 2025 following Fed rate cuts, although they remained higher than pre-pandemic levels. Rates changed last fall because the Federal Reserve began cutting its benchmark interest rate to support a softening labor market (higher unemployment) and stimulate the economy. This was a pivot away from the strategy of aggressive rate hikes used to combat high inflation in previous years.

- Based on current economic conditions and projections, rates are unlikely to move significantly more than they have over the last two years (barring a catastrophic economic event), remaining above 6% (the average rate over the last 50 years has been 7.7%).

What about values?

Texas urban real estate in 2026 is expected to experience continued stabilization, with a potential for slower price appreciation rather than a significant crash, as the market corrects from past rapid growth. (Double-digit appreciation usually is followed by the opposite…) Key factors influencing this trend will be mortgage rates, job market stability, and housing inventory levels. High inventory in some areas and high mortgage rates may provide buying opportunities, while the strong underlying economy of Texas continues to support demand, making a dramatic downturn unlikely. Key value trends to watch for 2026:

- Stabilizing Prices: Prices may stabilize or see minor growth after a period of rapid increases, but a significant decline is generally considered unlikely.

- Inventory Levels: A balanced market, characterized by 4 to 5 months of inventory, is considered a sign of a healthy market. Any increase in available homes can offer buyers more options and breathing room. Best ‘buyers’ market’ we have seen in 15+ years.

- Mortgage Rate Direction: Mortgage rates remain a key factor; falling rates would boost sales, while sustained higher rates will continue to affect buyer decisions.

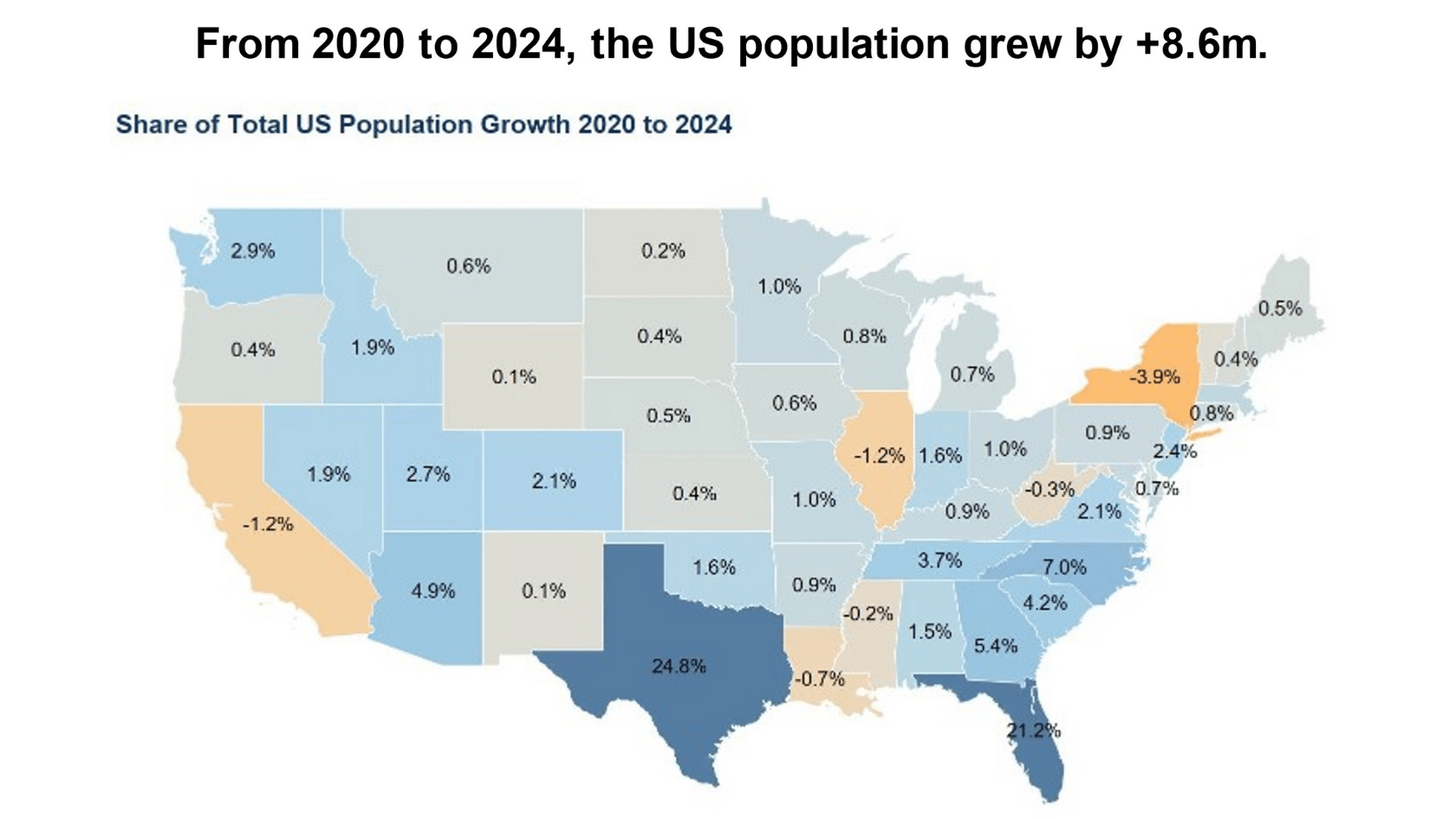

- Economic Fundamentals: Texas’s strong economy and job growth will continue to support demand and prevent the market from collapsing, although the days of automatic strong appreciation are over. Over 210 corporate or regional headquarters have relocated to Texas in the last five years. (That’s more than other states or countries.) The cost of building, including materials and labor, will continue to escalate. The lack of labor in all fields continues to be a challenge and is expected to persist for years due to a declining national population. (2033 is the actual year that the US deaths will outnumber births. Yes, the rest of the globe is experiencing the same thing with a few exceptions.)

- Local Market Variations: Predictions vary by local market, with some areas in our Texas metros experiencing slight declines in price, while others may see slight increases. Most listings are selling within 2% to 3% of the final list price.

What This Means for Buyers and Sellers:

- Buyers: A potentially stable market with higher inventory could create opportunities to find homes and negotiate better terms, especially in areas that have seen price corrections. Rates change frequently, so it is important to compare offers from different lenders to find the rate program that fits your family’s needs. Be aware that the Fed’s actions are not the sole factor determining your mortgage rate. Listen to the professionals: your Realtor, mortgage lender, inspector, and so on. They are not trying to steer you any other way except for the best value and opportunity.

- Sellers: Price correctly. We’re not in a cycle where homes “fly off the market” like before, and proper pricing and presentation will be crucial for sellers to attract buyers and complete sales. In most Texas metros, homes listed for under $4 million that remain on the market for longer than 90 days are likely overvalued by the seller and will require greater discounts to sell.

Should you wait for a better market?

Based on my 50+ years of evaluating real estate markets and economics, I believe values will continue to appreciate, and rates will remain stable. As I said earlier, you should have bought 5 years ago……..