How Federal Reserve Interest Rates Impact the Economy, Mortgage Rates, and the Real Estate Market

By Mark Sprague, Independence Title’s Director of Information Capital

What Is the Federal Reserve and Why Does It Control Interest Rates?

Stock markets react, and consumers delay their purchases whenever a politician speaks about lowering lending rates (especially if the speaker is the President).

Historically, elected officials eventually back down from such commentary, and the Dow Jones Industrial Average, the Standard & Poor’s 500, and the Nasdaq Composite Index all return to their recent “normal.”

As a political and economic issue, the Fed’s independence is likely to be a topic of lively discussion in the near term. Understanding the Fed’s role—and, more specifically, its independence—is essential to understanding how monetary policy shapes the broader economy. While often discussed in technical or political terms, the concept of “Fed independence” is fundamentally about ensuring long-term economic stability through data-driven decision-making not influenced by political pressures. And there is an inherent cost of lowering and raising rates, because money is not free.

A Brief History of the Federal Reserve and Monetary Policy

Congress established the U.S. Federal Reserve in 1913 following the financial panic of 1907, which exposed significant weaknesses in the nation’s banking system. The Fed serves as a central authority for managing monetary policy and maintaining financial stability. At its core, the Fed’s mission from Congress includes managing inflation, supporting maximum employment, and fostering conditions for sustainable economic growth. It accomplishes this through monetary policy—adjusting interest rates and controlling the money supply to influence economic activity. It’s important to understand the central bank’s history and its fiduciary responsibility to our nation.

The Great Depression and Early Monetary Policy Lessons

The Fed’s first major test came almost a century ago during the 1929 stock market crash. To curb speculation, the Fed tightened monetary policy by raising interest rates, a move now widely viewed as having exacerbated the economic downturn. This experience underscored the importance of flexibility and responsiveness in central banking. Subsequent reforms aimed to enhance the Fed’s independence, allowing it to respond more effectively to evolving economic conditions.

The Volcker Era and Fighting Inflation

The 1970s presented a particularly complex challenge: stagflation, a rare combination of high inflation and high unemployment. In response, Fed Chair Paul Volcker took bold steps in the early 1980s to raise interest rates significantly, triggering a recession but ultimately restoring price stability. The “Volcker Era” is often credited with laying the foundation for the long period of low inflation and steady growth that followed.

In 2008, during the global financial crisis, the Fed again played a central role—this time by implementing quantitative easing, an emergency measure in which the Fed injected liquidity into the banking system by buying bonds, mortgages, and other assets. The Fed took decisive steps again in 2020 in response to the COVID-19 pandemic, cutting interest rates to near zero and providing broad support to financial markets, in a successful effort to spur an economy that was near a standstill.

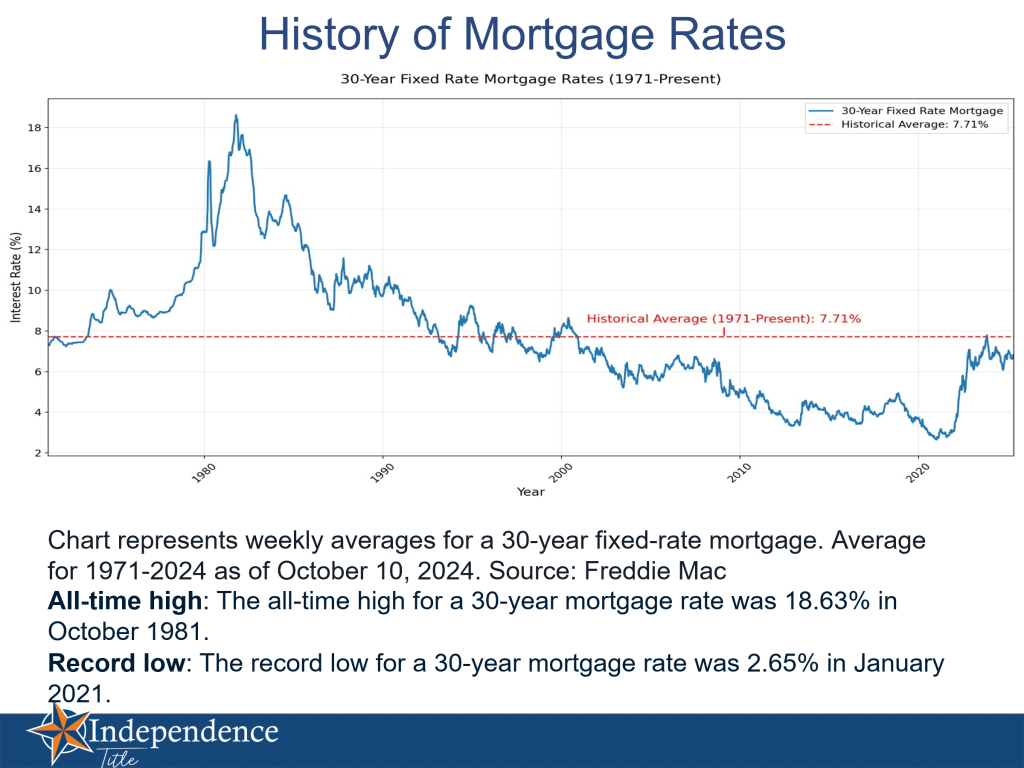

In lowering rates, we saw a surge in real estate sales (all channels ), other investments, and their values rising (20+% to 90% in 5 years). This is called an ‘asset bubble.’ A decline in borrowing rates usually stimulates the economy, raising the price of most assets and securities. Capital is cheaper to borrow, so more businesses expand, and more businesses are created. It’s easier to borrow for consumption, so businesses and people spend more. In housing terms, when you average 3.5% appreciation annually (as in our Texas housing metros), and then you have an annual surge into the 20+% to 30+% range, you have created a bubble. Bubbles are inflated by the future appreciation that would otherwise continue to rise in those housing markets.

But it’s more complicated than that for a few reasons. If interest rates fall due to declining inflation expectations, the expected cash flows from investments may decline as well, and borrowing is no easier. Also, if the economy slows, interest rates usually fall. While a fall in interest rates can mean an increase in asset prices, a decline in asset prices can cause a fall in interest rates. It’s hard to separate cause and effect in most cases.

However, as inflation surged in 2022, the Fed reversed course and raised interest rates rapidly to cool the economy and restore price stability. This was the first time in 50+ years that rates were raised without a recession.

The Importance of Federal Reserve Independence from Political Pressure

Throughout its history, the Fed has faced pressure from elected officials, particularly when economic goals conflict with political priorities and needs. In 1951, President Truman encouraged the Fed to keep interest rates low to manage post-war debt—a challenge that eventually led to the Treasury-Fed Accord, which formally established the Fed’s operational independence.

Similar dynamics reemerged in the early 1970s when President Nixon reportedly pressed Fed Chairman Arthur Burns to maintain low interest rates. The resulting inflation contributed to the stagflation crisis that Volcker later confronted. During the Reagan administration, political leaders again advocated for looser monetary policy, but the Fed maintained its stance. That steadfastness helped tame inflation over the long run. This dynamic also led to higher rates (up to 17+%) in the late 70s.

More recently, President Trump publicly criticized Fed Chair Powell—his own appointee—for not lowering interest rates quickly enough. This type of hyperbole is enticing and appealing to everyone’s greed. We all want cheaper money and greater equity growth. Then and now, for close to 100 years, there’s been speculation about potential changes in Fed leadership, highlighting the ongoing tension between the Fed’s autonomy and the preferences of elected officials.

The case against independence

There are several critiques of Federal Reserve independence. One primary concern is that the Fed is led by unelected officials who are not directly accountable to voters (a good thing, in this analyst’s view). Yet there are myriad examples in world history of countries that have gone or are going bankrupt because their central banks bowed to political pressure.

The Fed has also faced criticism for contributing to income and wealth inequality. Its use of low interest rates and asset purchase programs (such as quantitative easing) can inflate financial markets—benefiting wealthier individuals who hold more financial assets. In addition, the timing of the Fed’s policy interventions has occasionally been questioned. For example, some analysts argue that the Fed kept interest rates too low for too long after the 2000 market crash, potentially contributing to the housing bubble and the 2008 financial crisis.

Another critique is that Fed policy sometimes conflicts with fiscal policy set by Congress. For instance, the Fed may raise interest rates to curb inflation, even as lawmakers seek to stimulate the economy through increased government spending or tax cuts. (Lawmakers are looking to solve short-term issues, whereas the Fed is looking at long-term effects.)

Despite these concerns, it’s worth noting that countries with limited or no central bank independence—such as Russia, Argentina, Iran, Venezuela, Zimbabwe, and Turkey—have often faced persistent inflation, currency instability, and inconsistent economic growth. In contrast, most advanced economies—including the European Union, United Kingdom, Japan, Canada, Sweden, Norway, and Australia—maintain central banks with high levels of operational independence. These institutions are generally credited with supporting stable, long-term economic performance through data-driven, politically insulated decision-making.

The best argument for Fed independence?

Most importantly, sound monetary policy requires a long-term perspective. Economic cycles typically extend well beyond election cycles, and decisions about inflation, employment, and interest rates are most effective when driven by data rather than political considerations. Short-term solutions historically disregard the future. They want it, and they want it now.

An independent Fed allows for disciplined, consistent policymaking that anchors market expectations and supports stable financial conditions. Importantly, the Fed relies on extensive economic data from across the country to guide its decisions, a process that benefits from insulation against short-term political dynamics.

While the Federal Reserve is ultimately accountable to Congress and the public, its operational independence has always been a cornerstone of its credibility. The ability to make difficult but necessary decisions—even when they may be unpopular—is what enables the Fed to maintain long-term US economic health. Otherwise, politicians are constantly stepping on the gas and then the brake with no consistency or long-term vision. Inconsistency causes uncertainty and instability, which opposite of what is needed or wanted. Slow and steady.

As always, if you have any questions or concerns, please reach out.

MS