By Karen Burnett, Senior Vice President, Escrow Manager

FinCEN is part of the US Department of the Treasury that was created to help identify how some cash funds were being introduced into the US monetary system. Several laws already cover transactions involving banks and lenders (The Bank Secrecy Act and various anti-money laundering laws) so those transactions were not the target but there was a regulatory gap for real estate transactions involving substantial cash funds. No one was tracking real estate purchases in that manner, so FinCEN was created in part to help fill that gap.

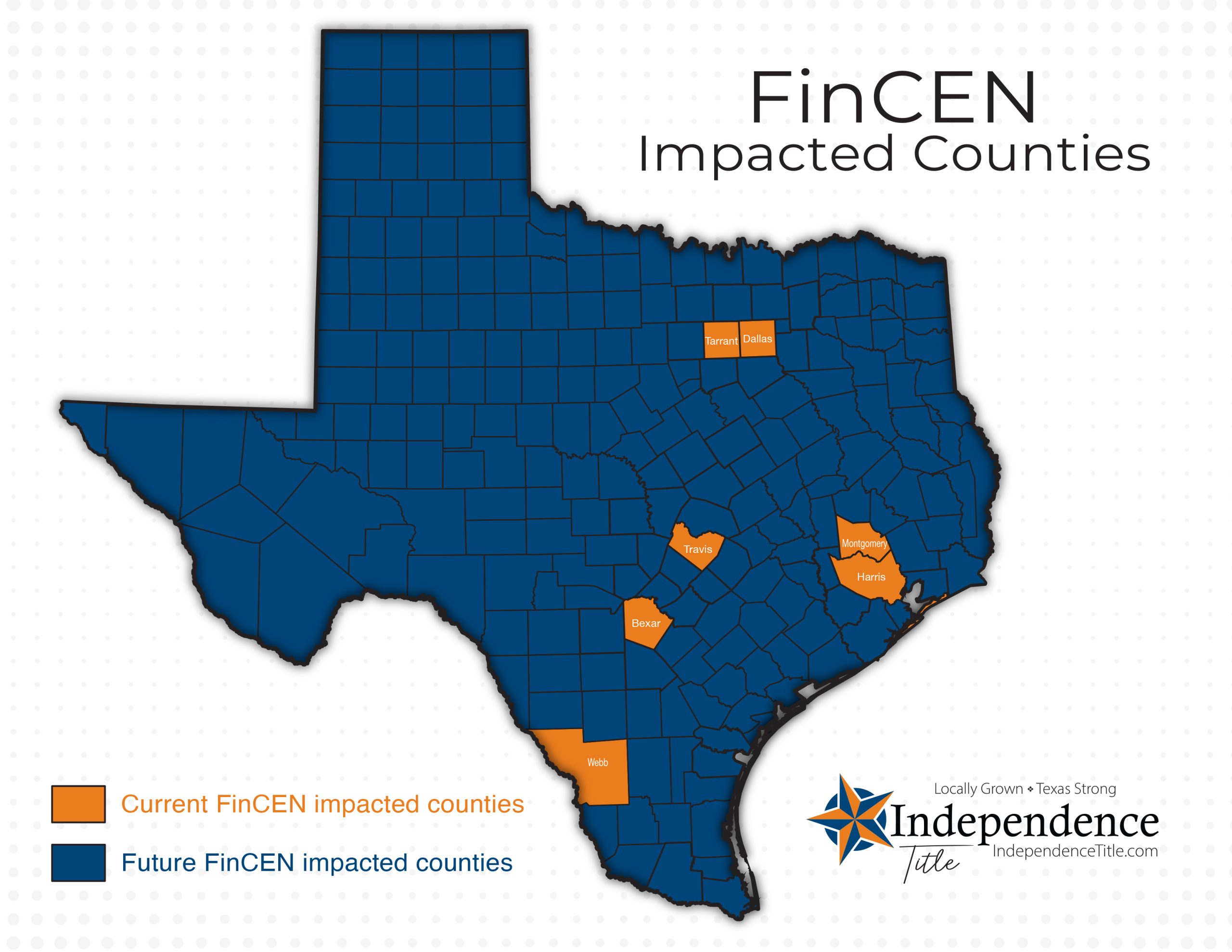

FinCEN originally started by reviewing select transactions in specific geographic locations, quickly expanding to cover 69 counties under what they call Geographic Targeting Orders or GTOs. These GTOs run for approximately six-month blocks of time and outline the criteria for what real estate transactions need to be reported. Different geographic locations have different sales price limits so we will solely focus on the counties impacted within the State of Texas.

For most transactions in Texas, the duty to report falls to Texas title insurance underwriters, who in turn rely on the title company closing the transaction for specific reports, and this is the reason we care about it. FinCEN requires that we, the settlement agent, on behalf of our underwriter, file a Currency Transaction Report or CTR on any transaction which meets the following criteria:

- Properties located in Bexar, Dallas, Harris, Montgomery, Tarrant, Travis, or Webb counties

- Residential property

- Vacant property with immediately contemplated residential improvements

- Sales price of $300,000 or more

- Purchaser is an entity*

- All cash purchases made with currency, certified check, wire, or virtual currency

- Purchases made with funds from a hard money lender or seller-financed funds

From the entity* buyer, the following information is needed for the report:

- Name of the entity

- Registered address of the entity

- TIN of the entity

- Formation documents/Articles of Incorporation/Operating Agreement/Partnership Agreements/Corporate Resolutions

For any member of the entity (FinCEN refers to them as beneficial owners) owning an interest of 25% or more in the entity, additional information must be collected from each beneficial owner:

- Name, address, and phone number of the individual

- Photo ID of the Individual

- SSN of the Individual

- Occupation

If the entity BUYER is a layered entity, for example a limited liability company (LLC) whose sole member is a corporation (Inc.), that owns 100% interest in the LLC, we will need to continue going down the line until we reach an individual owning 25% or more interest in the underlying company. In the event there is no individual who owns 25% or more interest in the company, we are then required to report information for the person who is primarily responsible for closing the transaction.

Obviously, identifying these transactions as early as possible is our best practice so that the required information can be gathered, reviewed and approved ahead of closing. Failure to provide or insufficient information may delay closing or possibly even prevent us from closing the transaction.

Contracts that meet all the criteria can be immediately addressed but amendments to contracts made after the contract is receipted by the settlement agent can cause problems. If you are preparing an amendment that changes any one of the criteria for FinCEN reporting, a transaction originally deemed non-reportable may become reportable. Common changes could include:

- Original contract comes in with an individual buyer but then changes to an entity buyer

- Original contract comes in with an entity buyer + financing but then changes to all cash

- Original contract comes in with a SP less than $300,000 but then changes to over $300,000

- TBD order opened with no buyer information; actual contract comes in with entity cash buyer

- Financing changes from traditional lender to hard-money or private lender, or seller finance

All the above information is the model under which FinCEN is currently operating but there is a proposed change coming Fall 2024 that expands the reach of FinCEN tremendously. Instead of only targeting certain geographic locations, the proposed FinCEN rule changes target ALL residential real estate purchases with an entity buyer made in cash, regardless of purchase price or geographic location. The definition of residential also potentially expands in their new model to include any vacant land zoned for residential use and vacant land zoned for mixed use such as retail space on the bottom floor and residential properties on the upper floors. In addition, certain aspects of the seller side will be included on the new reporting forms. These changes are under review and may be coming within the next 18-24 months. Our industry trade association, title insurance underwriters and industry leaders are working diligently to suitably amend these changes as we feel they create a significant burden on us as settlement agents.

In an even broader sweep and still down the line, FinCEN contemplates including commercial use properties. This is not in the current proposal but expected in the future.

If you have a transaction which you think may be subject to FinCEN reporting, please reach out to your favorite escrow officer for assistance.