By Mark Sprague, State Director of Information Capital

The Federal Reserve Bank’s policy-making committee (FOMC) raised rates this week (at the November 1-2 meeting) by .75% and kept a hawkish tone given the continued stream of inflationary data coming in since the September meeting. Inflation has slowed, but not much, and it may take a while to bring it under control.

Previously, it was expected the Fed would raise rates by .75% in both November and December meetings. The December hike is not off the table but may be less than expected. Presently, the Fed has shown no need for new economic projections to be released before the November meeting, so all the action will be in the FOMC statement and the Chair’s press conference.

A little good news … some of the Fed Reserve Governors have expressed interest in a smaller rate hike. Federal Reserve Chairman Jerome Powell is expected to highlight a wait-and-see stance about the December meeting decisions.

The contradictions in the U.S. economy keep piling up: economic output rebounded following two quarterly contractions, inflation remains stubbornly high, but unemployment is at historic lows. After six months of decline, the U.S. economy returned to growth in the third quarter. But there were also signs of a slowdown, as the factors underlying the 2.6 percent GDP growth aren’t robust enough to dispel recession concerns. Moreover, economists point to how the 2.6 percent increase in GDP in the third quarter had more to do with rising exports than anything else. So, the need for higher rates to slow inflation is still there.

Whatever scenario plays out (i.e., we avoid a recession, we have a recession, we avoid a recession in the near term, but it comes later, etc.), we’re in a very strange economic situation, which is bad news for economic officials fighting inflation. Prices, as well as wages, are still rising quickly. The combination of the rising cost of living and the Federal Reserve’s ongoing attempts to tackle it by hiking interest rates, which in turn strengthens the dollar and hurts exports, is still predicted to cause a recession.

I look at the overall factors and point out that as good as the Fed has been in the fight against inflation, it can’t control what is happening in China or eastern Europe. So, expect some kind of recession in the latter part of 2023. It will be different than any previous, with high net worths, higher incomes, no rise in foreclosures, not enough housing inventory (helping keep values strong), low unemployment (anything under 5% is considered full employment), more job openings than people out of work, etc.. 2023’s recession will be unlike any you and I have seen before.

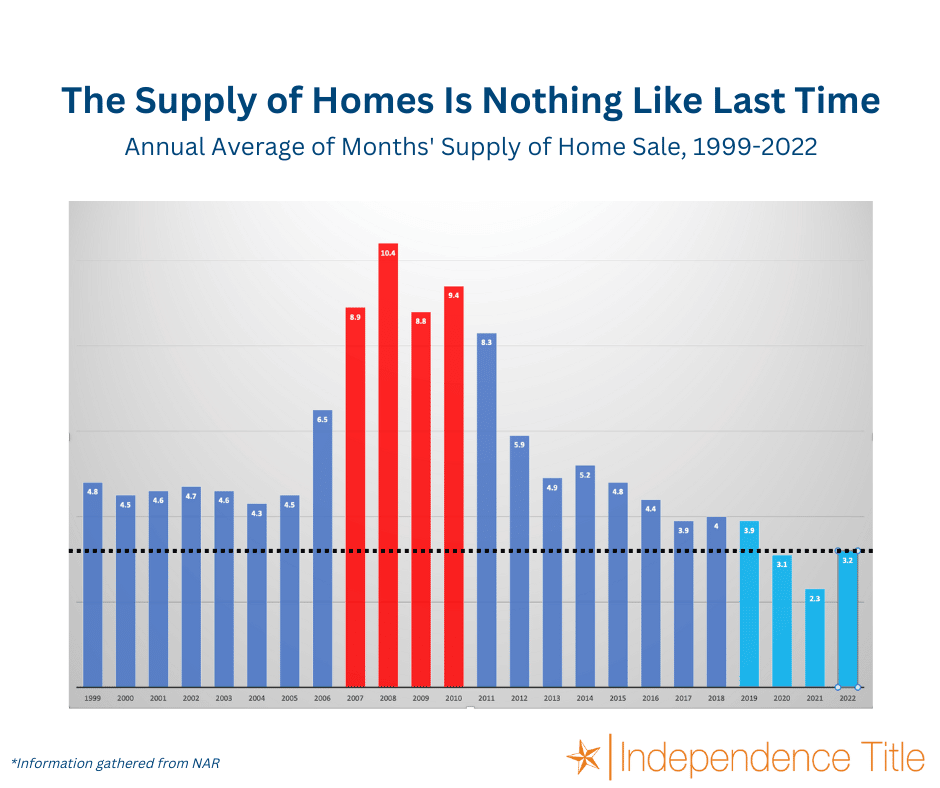

So, what does that mean to our clients in Texas? First, there is not enough housing inventory (for rent or sale) which, in turn, keeps values strong. The housing supply is still historically low. People with 3% mortgages (75+/- of America has mortgages less than 4%) will think twice about selling. Builders have put the brakes on the new supply of houses. Various factors will continue to put constraints on the supply.

Lending standards are not comparable to 2008, when anyone with a pulse and could fog a mirror could get a mortgage. Also, most people have substantial equity in their houses because lending standards are dramatically stricter than in previous recessions.

Foreclosures are still historically low. Compare today to the foreclosure rates running up to 2008. Not many homeowners nationally or regionally owe more on their mortgages than their property is worth. There is very little negative equity in the real estate channels presently.

It is appropriate that a real estate market on steroids like the last two years should cool down when you raise interest rates to slow inflation. It is expected and healthy. It doesn’t mean that house prices will drop.

For those clients that are waiting for rates or values to dip (as they have the last 30+ years, typically at signs of a recession), they will be sorely disappointed. Waiting to buy has already cost them 36% of buying power since the first of the year when rates were around. (Every time rates go up 1%, the buyer loses approximately 12% of buying power.) With projected rate increases through 2023, buyers will have lost 48% of their buying power by the end of the year. Possibly 60% buying power since the start of 2022. 72% buying power by the summer of 2023. Waiting for rates to come down will be harsh. Don’t expect those sub 4% rates again; that was a sign of a struggling economy.